The Power of a Comparative Market Analysis When Selling Your Home

Most of the general public has access to various price lists when trying to sell an object. Online automobile databases offer average prices for used cars, auction sites can list recent sale of various electronics and even boats have a value listing guide. However, when selling a home it is better to get a comparative market analysis (CMA) from a local real estate agent or Realtor®. Here are some of the ways a CMA can help you.

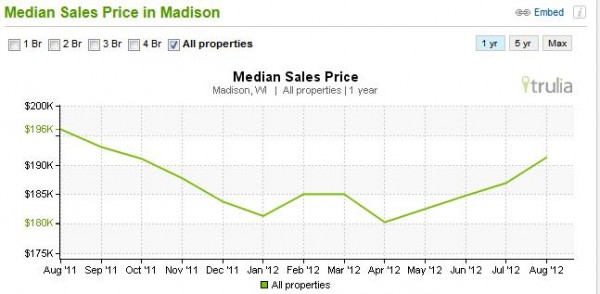

Price Trends

The most obvious benefit is the ability to see current price trends. The CMA report will list out homes that have sold in the past 12 months in your immediate area. By organizing the transactions by date it is possible to see if home prices are on the rise or falling.

Value Placed on Square Footage

Since the homes will be listed with the square footage of each home sold, potential sellers can find out how much their home is worth based on the usable square feet in the property. In addition, if any of the sold properties had a basement or attic that was finished then sellers can also determine how the market values additional square footage. While it is common for basements to have a slightly lower price per square foot some areas may place it higher than others due to demand.

Value of Accessory Items

Most people usually feel that particular features of their home will bring more value to their home than the market will warrant. For example, expensive hardwood floors, custom paint finishes and high end bathroom fixtures may be quite expensive when purchased but their overall impact on the price of a home is not as high. Instead, things that improve usable square footage, more lighting or outdoor items like pools and decks will do more to bring up the price of a home.

Expected Time of Sale

A comparative market analysis will also show when a home was listed for sale and when an offer was made on the property. This gives prospective sellers a realistic expectation for how long it will take before receiving an offer and how long it takes for the home to actually sell once the offer is accepted.

Avoiding Unrealistic Prices

Along with homes that have sold your real estate agent can also provide a list of homes that either withdrew from the market or the listing simply expired. If the home did not sell within a time period that multiple other properties sold then there are a couple of explanations. Obviously, the most common issue is the price was too high for that particular market. Another common problem is the presence of a major repair issue with the home that the seller is unwilling to fix prior to sale. Having this information should help you do a better job of picking a price for your home.

Getting a detailed CMA report from your real estate agent will provide you with the best source of realistic information to help you decide if your can sell your home for your anticipated price and if it might sell in the amount of time you had hoped for.

Original Blog Post: What's a CMA? Comparative Market Analysis

Give me a call for all your real estate needs, and let's make something amazing happen.

Give me a call for all your real estate needs, and let's make something amazing happen.