All Posts (60)

Sort by

Bad Choices People Make When They Buy a Home

All too often, people fall in love with a home for the wrong reason. And when it comes time to sell, they find that there are not as many people in love with the home like they were. Here are some common mistakes first time homebuyers make and how you can avoid the same errors.

Buy With Reselling in Mind

photo credit: woodleywonderworks via photopin cc

The previous generation considered a home purchase akin to a marriage; till death do us part. The new generation does not see it in such lasting terms. Modern families may move up in the value of a home, relocate to a better school district or simply sell what they have and move to a new state to pursue a different career. For people that buy a home with a small, or zero down payment, it will be tough to sell within a matter of just a few years. Staying in a home for a number of years gives the property time to appreciate while also giving you a chance to pay down the loan.

Older homes have lots of appeal to many buyers, but they also come with some major considerations. Modern appliances, up to date electrical systems and comfort due to a good air conditioning & heating system are usually not that common in older homes. You may purchase an old house with plans to improve these things as time goes along. However, if you find yourself in a position that you must sell before the renovations are complete, it may be tough to find a buyer.

Don’t Buy a Home Just on the Payment

Many would-be homebuyers look at the principal and interest payment for a proposed mortgage and say “I can handle that.” For the majority of these people, they are correct in their statement. However, they may be overlooking some major expenses.

First and foremost, a house is like a vehicle in the respect that it must be maintained in order to provide a long, useful life. Replacing the roof, getting new appliances, repairing the occasional plumbing problem, and a host of other items are just a part of owning a home. Homes that end up in foreclosure often show signs of neglect, mainly because the owner could not afford even the basic maintenance items.

Besides maintenance, there are property taxes as well as homeowner’s insurance. Depending on the location and value of the property, these two items can typically cost between $300 to $500 a month. Potential buyers need to do their homework and get a full estimate of their payments, along with escrow, from their lender.

Location

People that are novice to the real estate industry still understand one basic rule; location is king in realty. Homes located near shopping areas, close to good schools and exhibit low crime rates are the best selling properties. If you fall in love with a home and you are the only person considering the property, there could be a reason for the lack of competition. It is important to pick a home in a place conducive to an easy sell. Otherwise, you may be in for a long wait when it is time to get rid of the home in the future.

I just received notice that as of 1/15 BofA will no longer postpone the foreclosure process while a homeowner is working on a short sale.

This means that now, if the negotiations are not completed prior to the auction date of the property, they will sell it out from under them.

I thought that we resolved this issue with the Senate bill 306 here in ?California??

Has anyone else received this notice? Now what? Some days it feels like we are moving backward instead of forward...

If you are a Realtor or short sale negotiator who has done a short sale with Fannie Mae as the investor during the last few months, this blog post will likely raise a question or two. For  everyone else, it will definitely also raise an eyebrow or two. Government conspiracy theorists are certainly not a rarity in this day and age. Depending on who you speak to, many of our fellow citizens can come off as paranoid and irrational when speaking about all the secret plans they seem so sure our government and those in power are plotting and planning. While the theory I'm proposing on here is certainly not up to par with the New World Order, Illuminati, One World Government folks, it is certainly some concerning and valid food for thought, especially for those of us in the Real Estate and Mortgage industry. Take a few minutes to read this blog post, and you'll likely agree and come to find that this really isn't about a conspiracy theory, but a very real and disturbing trend that is happening in our housing market right now.

everyone else, it will definitely also raise an eyebrow or two. Government conspiracy theorists are certainly not a rarity in this day and age. Depending on who you speak to, many of our fellow citizens can come off as paranoid and irrational when speaking about all the secret plans they seem so sure our government and those in power are plotting and planning. While the theory I'm proposing on here is certainly not up to par with the New World Order, Illuminati, One World Government folks, it is certainly some concerning and valid food for thought, especially for those of us in the Real Estate and Mortgage industry. Take a few minutes to read this blog post, and you'll likely agree and come to find that this really isn't about a conspiracy theory, but a very real and disturbing trend that is happening in our housing market right now.

Lets take a step back here and set the stage. Over the last five to six years, we have seen real estate prices plummet in virtually every market across the country. This reality of the depressed housing market is certainly no secret. In many areas, prices have declined to as low as thirty cents on the dollar. Several years ago, As things became more and more depressed, our government stepped in. Both Fannie Mae and Freddie Mac, who back the majority of our residential mortgage loans, were completely bailed out by the US government. This forced overtaking was something that our government had to do, as the imminent collapse of Fannie and Freddie would have meant the complete collapse of the housing and finance industry, likely permanently. This was extremely important, as instead of giving bailout loans to Fannie Mae and Freddie Mac, like the auto industry or the banks, they actually took complete control of these organizations. Our government then established the Federal Housing Finance Agency (FHFA) to "oversee" these organizations which are now referred to as Government Sponsored Enterprises, or GSE's. Since then, the FHFA consistently dictates policy to these Government Sponsored Enterprises that still back most residential mortgage loans and completely control the secondary mortgage market.

they actually took complete control of these organizations. Our government then established the Federal Housing Finance Agency (FHFA) to "oversee" these organizations which are now referred to as Government Sponsored Enterprises, or GSE's. Since then, the FHFA consistently dictates policy to these Government Sponsored Enterprises that still back most residential mortgage loans and completely control the secondary mortgage market.

Now back to the present. Fantasic news headlines in much of the country that in many of the markets that were hardest hit, prices now seem to get going up almost as quickly as they were once declining. Inventories are low, demand is high, properties are getting multiple offers from buyers paying over list prices the minute they come on the market. But for those in the industry such as myself who are active in the short sale and distressed property niche, an interesting and disturbing practice that has been taking place.

![]() In very recent times, just in the past few months, short sale agents across the country have been having difficulties with Fannie Mae short sales. To be more specific, the difficulty has been with wildly inflated appraised property values that Fannie Mae has been insisting on for short sale properties. For those who may not know, we are not talking about regular appraisals, traditionally ordered by a buyers lender in order to justify a purchase price. In this case, we are talking about appraised values that Fannie Mae places on properties, ordered by them and completed by their own appraisers, utilizing their own appraising and property valuation methods. Utilizing these over inflated appraised values, Fannie Mae then demands more money for these short sale properties from patient buyers. Anyone starting to smell the stink yet? Does this stink smell a little similar to the stink we all experienced several years ago with inflated buyer appraisals from before the housing market collapse?

In very recent times, just in the past few months, short sale agents across the country have been having difficulties with Fannie Mae short sales. To be more specific, the difficulty has been with wildly inflated appraised property values that Fannie Mae has been insisting on for short sale properties. For those who may not know, we are not talking about regular appraisals, traditionally ordered by a buyers lender in order to justify a purchase price. In this case, we are talking about appraised values that Fannie Mae places on properties, ordered by them and completed by their own appraisers, utilizing their own appraising and property valuation methods. Utilizing these over inflated appraised values, Fannie Mae then demands more money for these short sale properties from patient buyers. Anyone starting to smell the stink yet? Does this stink smell a little similar to the stink we all experienced several years ago with inflated buyer appraisals from before the housing market collapse?

For the most active short sale agents across the country, the past few months have produced quiet a few headaches with Fannie Mae. It seems virtually every property valuation and appraisal done by Fannie Mae for a short sale is at least 10% or more above current market value. Values so inflated, that there are typically no comparable sales at all to come remotely close to justifying their prices. Prices so high, that it most cases it would be virtually impossible for a buyer to find a loan and get an appraisal that would match the property values and prices that Fannie Mae is demanding. The ironic part, is that these same buyers' loans who are purchasing these properties would of course eventually be sold off to... You guessed it, Fannie Mae! Because of the massive number of loans backed by Fannie Mae, this is widespread and is effecting a very high percentage of current sales. And when it comes to disputing these inflated values, it can be quiet a challenge for real estate agents and short sale processors to convince Fannie Mae to change their mind and sell the properties for actual market value.

For the most active short sale agents across the country, the past few months have produced quiet a few headaches with Fannie Mae. It seems virtually every property valuation and appraisal done by Fannie Mae for a short sale is at least 10% or more above current market value. Values so inflated, that there are typically no comparable sales at all to come remotely close to justifying their prices. Prices so high, that it most cases it would be virtually impossible for a buyer to find a loan and get an appraisal that would match the property values and prices that Fannie Mae is demanding. The ironic part, is that these same buyers' loans who are purchasing these properties would of course eventually be sold off to... You guessed it, Fannie Mae! Because of the massive number of loans backed by Fannie Mae, this is widespread and is effecting a very high percentage of current sales. And when it comes to disputing these inflated values, it can be quiet a challenge for real estate agents and short sale processors to convince Fannie Mae to change their mind and sell the properties for actual market value.

Put two and two together, read between the lines, and it makes perfect sense that this is just Fannie Mae's and our policy dictating governments' valiant and likely effective attempt at mass, government controlled real estate price fixing. Control the supply (market inventory), control the demand (interest rates ect), and then control prices and force up property values by demanding more money. Fannie Mae and Government controlled real estate price fixing. The tail wags the dog, and the dog has no clue what is going on. A perfect example of the reality that housing has become completely socialized, but with the illusion that its just all part of the market cycle. Just my two cents, for what its worth.

Click Here for my original article on Government Real Estate Price Fixing

Rock Realty Client Testimonials

"I had a very challenging home sale and Mike Collins was diligent every step of the way. The most difficult aspect may have been me, I was very specific about which closing dates worked and how I wanted to proceed. Mike patiently answered all of my questions and accommodated all of my requests. When issues between the title and mortgage companies arose, Mike was a swift and competent negotiator. I know that the buyer's agent was very impressed with Mike as well. My house had an accepted offer within 10 days of listing. I am amazed that it all went so smoothly. THANKS MIKE!"

John B.(Madison, WI)

Rock Realty Seller Client

![]()

Thanks for the compliments, and Congratulations on your closing John!

photo credit: QuidnuncQuixot via photopin cc

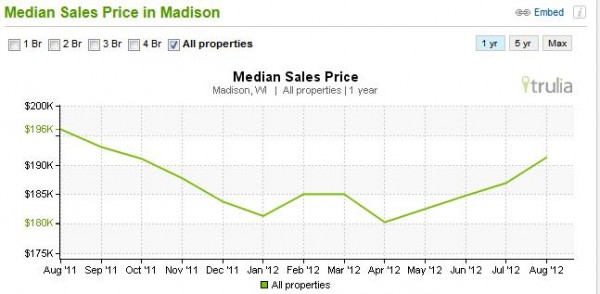

Home Prices in Madison Show Improvement

Lots of good news about the Wisconsin real estate market has come out over the past two months. Home prices are beginning to improve, homes are selling a bit quicker and foreclosures are down. All of this points to improvement in the real estate market. Listed below are some facts about prices in Madison based on various parameters.

Overall, home prices have been growing steadly since April of 2012. The following chart, provided by Trulia, shows the average sales price across all types of homes

Although home prices have not returned to the average of $196,000 like it was last year, it is getting close. When comparing home prices at different tiers, Madison is staying ahead of the rest of the state in all three tiers. The following charts are from Zillow. This first chart points out two facts. First, the average price for a home in Wisconsin in the upper tier is around $232,000. However, for Madison the price is approximately $295,000. This points to the continued growth in the Madison area. Secondly, while the average price in this tier only increased 0.2% for the state of Wisconsin, in Madison the price improved by 1.6%

For the middle tier pricing, the average price in Wisconsin is $142,000 compared to $187,000 in Madison. This tier has also seen an increase from the last quarter, although not as strong as the higher tier.

Although the bottom tier in Madison has not shown as strong a price increase as the rest of the state, it is still moving up, which is a good indication.

When looking at homes based on size, there is even better news all around. Homes at every size in Madison have shown increase in value over the past few months, as evidenced by this chart from Trulia.

No. Bedrooms | May - Jul '12 | 3 months prior | 1 year prior | 5 years prior |

1 bedroom | $156,200 | $145,000 | $166,000 | $167,000 |

2 bedrooms | $165,000 | $141,500 | $155,000 | $172,250 |

3 bedrooms | $185,000 | $180,000 | $194,250 | $210,000 |

4 bedrooms | $239,500 | $232,250 | $245,000 | $267,500 |

All properties | $191,250 | $182,500 | $196,000 | $204,900 |

Based on these figures, the average price across all home sizes has increased an average of 4.5% in the past three months.

Large log home on 38+ Acres listed $140k below assessment! Short Sale property.

N4587 Glacier Lake Dr, Oxford, WI 53952

Now just $225,000! We are already getting calls from serious buyers because of this huge price drop! 38+ acre hunters paradise for an absolute steal. This is truly a must see. Log home with Brazilian rosewood flooring, stone fireplace in living room, and master bedroom in loft with walk-in closet. Exposed finished basement with large full bathroom. Yurt structure with electric, water and wood burning stove. 7 Lakes within 5 minutes of property. Don't let this deal pass you by.

Now just $225,000! We are already getting calls from serious buyers because of this huge price drop! 38+ acre hunters paradise for an absolute steal. This is truly a must see. Log home with Brazilian rosewood flooring, stone fireplace in living room, and master bedroom in loft with walk-in closet. Exposed finished basement with large full bathroom. Yurt structure with electric, water and wood burning stove. 7 Lakes within 5 minutes of property. Don't let this deal pass you by.Features

Bedrooms: 3

Bedrooms: 3- Bathrooms: 3

- Home Size: 2,928sq.ft.

- Lot Size: 38.8 Acres

- County: Marquette

- Property Type: Single Family Home

- Year Built: 2005

- MLS Number: 1667732

Property Highlights

Wooded Acreage

Wooded Acreage- $140,000+ below assess

- Wrap-Around Porch

- Brazilian Hardwoods

- Walk-In Shower

- Loft

- Hunting Paradise

- Close to Lakes

- Yurt

- Stone Fireplace

- Wood Burning

- Walk-In Closet

- Finished Basement

- Almost 39 Acres

- Privacy

- 3 Bathrooms

- Tiled Bathroom

Good morning Superstars.

Here's a sampling of this week's Superstar discussions.

Junior Lienholder Arms LengthMy wife and I are trying to purchase a home that is very near and dear to us which is currently in a short sale/foreclosure status. I am… Started by Rich Jenkins in Short Sale DiscussionsLatest Reply |

Short Sale versus Foreclosure waiting times for new purchaseHere is a list of timelines for Government loans when purchasing a new home. SHORT SALE AND FORECLOSURE WAITING PERIODS FHA /VA Conve… Started by Ron Scribner in Short Sale DiscussionsLatest Reply |

Fannie Mae Valuation - Call updateI'm sure many of you are anxiously waiting for information regarding the results of the conference call set up to discuss issues with Fanni… Started by Ken Ryan in Short Sale DiscussionsLatest Reply |

Locksmiths in Spain Revolt! This is so great....Compared To Spanish Locksmiths, Americans Have Lost Their Cojones by Steve Dibert in HPN Blog inShare0 Iker de Carlos, a 22 year old… Started by Wendy Martin in Short Sale DiscussionsLatest Reply |

Does a discharged bankruptcy affect a sellers incentive?Hey Superstars, I have a question, just like the title states does a discharged bankruptcy affect a seller in receiving a incentive from t… Started by Freddie Castaneda in Short Sale DiscussionsLatest Reply |

2013 Short Sale Symposium at Sea Cruise Conference April 20th-25th!Are you coming to see me and join many of the best minds in the industry at the 2013 Short Sale Symposium at Sea Conference? You des… Started by Mike Linkenauger in Short Sale DiscussionsLatest Reply |

7 Tips To Help Ensure The Short Sale Buyer Stays On BoardGood morning Superstars. So you have been working for 4 months to receive short sale approval only to have the buyer walk. As a short sale… Started by you in Short Sale DiscussionsLatest Reply |

Is Selling The Short Sale To The Tenant A Good Idea?In my opinion.....no...it’s not. And here’s why. The Lenders want as much money as possible for the property. They want the property e… Started by you in Short Sale DiscussionsLatest Reply |

Do You Need More Short Sale Listings?

Short Sale Superstars wants to make generating Short Sale leads easier for you. So.....we have partnered with the Short Sale Specialist Network to offer you.....

AND......if you use coupon code SUPERSTAR you will get an additional month for only $1. That means you can have your site set up and use it for two months for only $2!

PLUS.....here is a FREE one hour course on Short Sale Lead Generation that may help you.

Let's make 2013 a banner year for Short Sales. Together we can help a lot of folks avoid foreclosure.

***Don't forget to use coupon code SUPERSTAR for the additional discount.

LAKE ELSINORE CA SHORT SALE REALTORS

Lake Elsinore CA Short Sales Made Easy…

You Pay Nothing For Our Lake Elsinore CA Real Estate REALTOR Services!

SHORT SELL THAT LAKE ELSINORE CA HOUSE NOW! CALL: 1 (888) 9 LIST-IT

-Is your Lake Elsinore CA house worth less than you owe?

-Having trouble paying your Lake Elsinore CA mortgage or are you already behind?

-Have an Adjustable Rate Mortgage, or a Negative Amortized Loan?

-Are you concerned about tax implications? -Do you have questions about how short sales work?

Many Lake Elsinore CA home owners are short selling their upside-down Lake Elsinore CA properties and so can you!

We are Certified Foreclosure & Short Sale Specialists and we can help you sell that upside-down Lake Elsinore CA House!

YOU PAY US NOTHING CALL NOW: 1 (888) 9-LIST-IT

Or email us at:

We also handle:

-Lake Elsinore CA Standard Sales

-Lake Elsinore CA Foreclosures

-Lake Elsinore CA Property Sales

-Lake Elsinore CA Home Buyers

This is not a HAFA short sale, but they have been told they will receive relocation money.

I have a short sale in progress and my seller is being sent drive by fee's from the lender.

every two weeks or so the lender (Seterus) has someone drive by the home. Then a bill is sent to my seller.

Has anyone encountered this before? What if anything should my seller do?

The SMART Way to Buy Your First Short Sale

Buying a short sale in Madison Wisconsin is quite common right now. The impact of the financial recession has resulted in numerous foreclosures and has left some people with no option but to sell their home for less than the mortgage balance. Buying a Madison area Wisconsin short sale will require a bit of patience and a smart plan.

Understanding the Short Sale

Obviously, the best reason to buy a short sale is for the savings. Most of these properties are discounted as much as 20% off the market price. Buyers can save a considerable amount of money by negotiating the right deal with a motivated seller. However, a good price should only be one consideration. There are other things for the buyer to be aware of such as:

* In order to get a contract on a short sale, it is best to be the first person to contact the seller or selling agent. Being first puts you in more control of the transaction.

* Just because a property is being offered as a short sale does not make it a great deal. Some properties may need extensive work before they can be deemed a safe living environment.

* Banks typically frown on ridiculous low offers. A successful short sale will require you to offer a reasonable amount. This is where an agent can really come in handy.

* Based on the current number of short sales, banks are swamped with these requests. The process for moving the offer through the chain of command does not always progress in an orderly fashion. This requires the buyer to be flexible about a closing date.

All of this means that buying a short sale requires a solid plan; a plan that will get you in front of the right seller, with the right offer.

Putting Together a Good Plan

Follow this outline to help you develop a plan for buying your first short sale.

1. First and foremost, you need to meet with a real estate agent that has experience in short sale transactions. This will save you lots of time and trouble throughout the process. The agent can have a conversation with you to determine the type of house you need and look for possible short sale targets.

2. Determine a plan for responding when a short sale becomes available. Decide with your agent how the information will be communicated to you and how soon you can look over the home.

3. Set up a meeting with a local mortgage lender. Getting the financing secured ahead of time will help get your offer approved. A lender that is familiar with short sale transactions would also be beneficial since the closing may happen at any time and the lender will need to be prepared.

Understand that a short sale which seems like a good deal will likely draw attention from several buyers. The person that responds the quickest, with the best offer and the best plan in place, will likely win the bidding war.

Inexpensive Ways to Boost Your Home’s Value

Although mortgage rates are still at an all-time low, there are lots of homes on the market for potential buyers to choose. This makes competition tougher for sellers. If you are in the market to sell a property, it might be wise to take some time and spend a few dollars on simple things that will yield great results.

Choose the Right Agent

Sometimes the most important thing for a home seller is the most overlooked. Get a real estate agent that is good for you. There are numerous agents available, all with various personalities, strengths and weaknesses. Here are some tips for finding an agent that you are comfortable with and can help move your property.

* Visit a few open houses: This will give you a chance to see the agent interact with other interested buyers. You can gauge their professionalism, demeanor and overall knowledge of the market.

* Ask your friends and family members for a referral: This can be an easy way to find a Realtor®, but use a bit of caution. An agent that has lots of experience selling country homes with acreage may not be the best choice to sell your suburban 3 bedroom home. Make sure to check out their other sold listings and see how many are comparable to your place.

* Do an online search: Check out agents online. Look for their website and do a little research. Is their site professional looking? Is it updated with current listings? How well do they explain the homes they are trying to sell now? Are there lots of pictures? Once you have found someone you like, give them a call and do a brief interview over the phone.

Paint

Paint

One of the quickest and cheapest ways to alter a room's appearance is by simply adding a fresh coat of paint. Most any able bodied person can work a roller and a brush. Choose a color that is a bit neutral but also bright so that it will make the room livelier.

Clean up and Streamline

Obviously, you want the home as clean as possible. Take extra care to clean the bathrooms and kitchen. Also spend some time organizing and getting rid of clutter. Remove any excess wall hangings. This will make the room feel more open and larger. Making a home inviting and spacious will attract more buyers.

Improve the Curb Appeal

Improve the Curb Appeal

Like painting, this will likely involve more sweat than money. If you have shrubs make sure they are trimmed and neat. Give the lawn a fresh cut. Put a new welcome pad by the front door. Also, include some type of attractive plant near the front door. Since this area will likely be prominent in pictures that are trying to sell the home you want it to look inviting.

Bridging Outdoor Areas with Inside Areas

Use decorative plants around the patio and deck as well as inside the home. Use comfortable furniture outside that has soft cushions. This makes the home feel bigger with more usable space outside that can be used in a number of situations.

Changes in Popularity of Features in New Homes

The national economy runs through cycles similar to the fashion industry. Things that seem irresistible and trendy this year may be old news by the time next year rolls around. As a result of the economic down turn from the past few years most home builders are turning their attention to items that are practical instead of luxurious.

Sunrooms

As a whole, sunrooms are declining in popularity. According to Rose Quint, a representative of the National Association of Home Builders (NAHB) “Builders are focusing on features that add immediate value and make a home more practical.” For example, most builders are choosing to add linen closets and walk-in closets in place of a sunroom.

As a whole, sunrooms are declining in popularity. According to Rose Quint, a representative of the National Association of Home Builders (NAHB) “Builders are focusing on features that add immediate value and make a home more practical.” For example, most builders are choosing to add linen closets and walk-in closets in place of a sunroom.

Separate Living Room

Most builders feel that a formal living room will not be very prevalent in new construction for the upcoming year. Families would prefer to have one giant open area that encompasses the living room, dining room and kitchen.

Media Room

Along with the living room, the media room will also likely disappear. The extra cost of the equipment, along with heating and cooling another room that is used sparingly, is just not appealing at this time. What is more likely to appear in new homes is a hidden away station that holds all of the DVD players, cable controls and charging stations for cell phones, tablets, and other media devices.

Two Story Family Room and Foyer

Since builders are approaching new homes with more practicality, it makes sense to cut down on unused space. While a family room may be bigger in new homes to include the dining and kitchen areas, it is unlikely to be two stories tall. The same goes for the elegant foyers that stretch toward the sky with large windows. Both of these features of a home may be lovely in appearance, but they each have a lot of space that is not used by a family of four or more.

Whirlpool Bathtubs

A large tub designed for relaxation and luxury is less likely to part of a new construction in the upcoming year. A separate tub laid out in a classic style is more useful and can be used to make a fashion statement while also having an everyday use.

Luxury Bathroom

Large bathrooms that include walk-in showers and multiple shower heads, as well as lots of floor space, will be harder to find in a new house. Instead, the shower will be smaller, with a single head, and the kitchen will likely include a double sink.

Outdoor Kitchen

The outdoor kitchen will probably disappear from lots of new homes. While it can be a nice place to gather with friends or family for a birthday party or to watch a football game, it also requires having an extra appliance or two. Most families would rather prepare the food inside and simply transport it to the patio and save on the cost of the additional appliances.

The outdoor kitchen will probably disappear from lots of new homes. While it can be a nice place to gather with friends or family for a birthday party or to watch a football game, it also requires having an extra appliance or two. Most families would rather prepare the food inside and simply transport it to the patio and save on the cost of the additional appliances.

Assuming an Existing FHA Loan

Most mortgages have a requirement that the loan must be paid in full when the property is sold. However, FHA offers a different option to the seller and buyer. It is possible for the buyer to take over the existing FHA mortgage from the current property owner. This is a very enticing offer for someone that has a mortgage with a great interest rate. Here are the guidelines for an assumable FHA mortgage.

photo credit: 401(K) 2012 via photopin cc[/caption]

photo credit: 401(K) 2012 via photopin cc[/caption]

Review Existing Loan

The first thing you should do as a potential buyer is review the existing loan documents. Any loan that originated prior to December 1 in 1986 is allowed to go through a “simple assumption” procedure. This means the buyer does not have to qualify for the FHA mortgage. For loans that were originated on after the December date, the buyer will have to qualify for the loan just like any new borrower.

Negotiate a Price with the Seller

Most sellers would like to receive a large part of the equity they paid in to the mortgage over the years since they originated the loan. The price you can negotiate is really dependent on your ability to deal and the seller’s motivation for getting rid of the home. One thing that must be clear; the buyout amount given from buyer to seller cannot be financed in to the existing FHA mortgage. This is money that needs to be paid either in cash or with a loan separate from the mortgage.

It may be possible to convince the seller to finance the buyout amount. This would mean that you have two loans to repay in order to purchase the home.

Talk to a Mortgage Lender

Since you will likely have to qualify for an FHA mortgage loan, it is advisable to talk to a lender experienced with FHA loans. The lender can review your credit file, determine your monthly income per FHA guidelines and find out if you qualify for the loan.

Determine Current Loan Status

You need to find out if the current property owner is up to date on their mortgage payments. If there are any late payments, those payments are transferred to the new buyer. This can be rectified by either paying the amount necessary to get current or requesting a modification of the loan.

Inquire About Down Payment

Since FHA asks for a down payment equal to 3.5% of the price, this rule will apply to someone assuming the loan. In this case, the 3.5% is based on the existing loan balance.

If you are approved for the loan, you may proceed with the closing process. You should ask the lender to contact a local title agency to research the title to ensure there are no liens on the property other than the FHA mortgage. Additional liens will have to be paid in order to transfer the deed in to your name as owner.

This communication is provided to you for informational purposes only and should not be relied upon by you. Rock Realty is not a mortgage lender and so you should contact a lender directly to learn more about its mortgage products and your eligibility for such products.VA Mortgage Program Has Good News for Veterans and Their Families

Photo credit: Tony Fischer Photography via photopin cc

Photo credit: Tony Fischer Photography via photopin cc

Many years ago the United States decided it was a good idea to offer housing benefits for our veterans that were not attainable to other classes of people. The men and women who sacrificed time away from their families and risked their lives in defense of our country deserved the chance to buy a home with attractive features. As time has marched on and the needs of veterans have changed, the VA Mortgage program has made some changes to appeal to even more qualified borrowers.

Spouses of Deceased Veterans

Before the new law, spouses of deceased veterans could only apply for a VA mortgage if the veteran passed away during active duty defending our country or if the veteran passed away due to a disability sustained during duty. However, if the spouse can show that the veteran suffered from a disability sustained during duty for a minimum of 10 years prior to their death, the spouse can now apply for the VA mortgage.

Funding Fee for Certain VA Loans Waived

People in the military are no stranger to paper work. With every VA loan that is approved there is a fee associated with the loan. This funding fee provides money for the new crop of loans, avoiding the use of taxpayer's money.

If a veteran learns that they are eligible for disability pay due to their physical exam prior to discharge then they are allowed to waive the funding fee from the VA mortgage. Previously, a veteran had to receive actual disability pay on a regular basis before the fee could be removed.

Beyond Fixed Rate Loans

Fixed rate mortgages are great for people who are reasonably confident that they will stay in a certain home for many years. Having the mortgage payment set in stone offers stability for the homeowner. However, there are some people, such as veterans and active duty personnel, which may be on the move in a few years. For these people, getting an Adjustable Rate Mortgage (ARM) can make sense. They save money by getting a slightly lower interest rate that is fixed for 3 or 5 years. The new law makes it possible for eligible borrowers to apply for an ARM through the VA mortgage plan.

More Flexibility for Military Families and Individual Parents

For as long as the VA mortgage program has been around, one of the main requirements to the loan has been the veteran's occupancy. A VA loan states that the veteran must live in the home as their primary residence after the loan is completed. The veteran is given some time to move in to the new home, but the requirement is there. For military families in which both spouses are active duty, this can be impossible. Even harder for families that have only one parent who is serving in the military.

The Camp Lejeune act makes it possible for the children of the veteran to meet the requirement of occupancy. This means that dependents can live in the home purchased by their parent or parents through the VA mortgage while the parents sacrifice their time away from loved ones serving our country.

This communication is provided to you for informational purposes only and should not be relied upon by you. Rock Realty is not a mortgage lender and so you should contact a lender directly to learn more about its mortgage products and your eligibility for such products. The Wisconsin housing statistics are now in for November of 2012. Here is an excerpt from what the Wisconsin Realtors Association (WRA) had to say:

The Wisconsin housing statistics are now in for November of 2012. Here is an excerpt from what the Wisconsin Realtors Association (WRA) had to say:“With 17 straight months of healthy growth in statewide home sales, there’s no doubt that the state housing market has seen a real bounce this year," said Renny Diedrich, chairman of the WRA board of directors. She pointed out that the year-to-date sales are up 21.2 percent, which is by far the highest levels seen since 2007, just before the recession officially began.

“The decline in the median price in November follows a relatively strong uptick in October, so it’s difficult to say precisely what caused this volatility, but year-to-date, median prices are still up,” said WRA President and CEO, Michael Theo.

Below are the number of Home Sales and Median House Prices for the state of Wisconsin, Rock County, and Dane County. These stats include Janesville and Madison. Feel free to contact me if you have any questions pertaining to these figures. As you probably have heard, home sales have been increasing substantially all year. That was still the case in November 2012. Although statewide, home prices have increased, in Dane & Rock counties, they are still decreasing in price.

If you would like some insight into how much your home is currently worth, I would be happy to provide you with a free comparative market analysis. This is a report that gives a close estimate to what your home might sell for in your current local Wisconsin real estate market. Has your home value fallen below what you currently owe? A short sale may be right for your situation. Visit the following page on Wisconsin Short Sales.

Housing Statistics for the State of Wisconsin:

November 2012

Home Sales: 5,030

Median Home Price: $129,000

November 2011

Home Sales: 3,956

Median Home Price: $133,000

Housing Statistics for Dane County, WI:

November 2012

Home Sales: 412

Median Home Price: $195,000

November 2011

Home Sales: 342

Median Home Price: $210,405

Housing Statistics for Rock County, WI:

November 2012

Home Sales: 143

Median Home Price: $86,000

November 2011

Home Sales: 117

Median Home Price: $95,000

View my report from last month. Wisconsin October Housing Statistics

If you are the Personal Representative for a San Bruno Home in Probate that has a delinquent mortgage, but there is equity in the home, DON'T BE AN OSTRICH!!!!!!

It is now very common for San Bruno homes that are in Probate to have mortgages. Many homeowners were enticed to refinance in the last decade because of easy money or low interest rates, many seniors have reverse mortgages on their San Bruno Probate homes, and some people did not refinance because of low interest rates, but because they were helping out family members.

When a mortgagee dies the mortgage still needs to be paid. Death does not eliminate the obligation. So what do you do if the mortgage is late, the home is in foreclosure, and the estate has no money to pay the mortgage? It is very common for San Bruno Probate estates to be house rich but cash poor.

The first thing that has to happen in a probate with this situation is that a personal representative needs to be appointed. This sounds like a no brainer, but sometimes there are fights within a family as to who that person is going to be, and while people are fighting the bank could be foreclosing. So stop fighting and get someone appointed.

Once the Personal Representative is appointed he or she should hire a real estate agent. This agent should have experience in both probate and short sales. Probate experience is a no brainer, but the reason for short sale experience is because that person will know who to talk to to postpone the foreclosure.

You will need to give authorization to your agent to speak with the bank and that takes a few days, so do this right away.

Once the postponement is granted get your San Bruno Probate home on the market and get it sold. Postponements generally are only good for 30 days at a time, and you may not get a second one if the home does not have an offer, so don't delay.

If the home has no equity then you should speak with the bank about a Deed in Lieu of Foreclosure. You may be able to negotiate the bank giving the estate $5,000 to $10,000 if you give them the keys and empty out the San Bruno Probate home. However, prices are appreciating so rapidly right now that you may believe your San Bruno Probate home is underwater when it really isn't.

So, if you have a San Bruno home in Probate and there is no money to pay the mortgage, don't just stand there, do something. Take the necessary steps to get help to make sure the estate's home is not lost to foreclosure. If you hide your head you could lose hundreds of thousand of dollars in equity.

If you have any questions about selling a San Bruno Home in Probate please feel free to contact me.

Marcy Moyer

marcy@marcymoyer.com

D.R.E. 01191194

650-619-9285

We are happy to announce the closing on another one of our short sale listings, this time in Madison, WI! This was a Bank of America negotiated short sale. Bank of America has made many changes to make their short sale process easier and more efficient. Short sale transactions can be complex, but if you have an experienced Short Sale Realtor® the process is much more manageable.

We are happy to announce the closing on another one of our short sale listings, this time in Madison, WI! This was a Bank of America negotiated short sale. Bank of America has made many changes to make their short sale process easier and more efficient. Short sale transactions can be complex, but if you have an experienced Short Sale Realtor® the process is much more manageable.

This was a beautiful home, at a great price that the new owners are sure to enjoy! If you are thinking of selling or buying a short sale home in Wisconsin, our short sale specialists would be happy to assist you. Give Rock Realty a call at 608-921-8536.

Is a Short Sale right for my situation??

If you are considering the possibility of a short sale for your home and have further questions, feel free to visit the page below:

Beaumont California Real Estate Short Sales - Beaumont Short Sale Agents Can Sell Your Upside-Down Home - Call Us Now: 1 (888) 9-LIST-IT

Are you like many homeowners in Beaumont having trouble paying your mortgage every month? You may be behind in your mortgage payments, or not behind yet. Don't let foreclosure happen to you. Hire the best Short Sales Experts to help you with your difficult situation at NO CHARGE TO YOU!

We are Short Sale Specialists and we have extensive experience with short sale negotiations with dozens of the nation's mortgage lenders and banks. Whether you have one, two or more Beaumont mortgage loans, we are able to offer you options. Our Short Sale Agent team assists homeowners throughout Southern California, including Beaumont.

Here are a few things to consider when contemplating a Beaumont CA Short Sale:

- How many loans do you have on the property?

- Do you or the property have any liens attached, for example: Tax liens, child support liens or HOA liens, etc.?

- Have you or your family experienced a loss in income, loss of a job or had to relocate for a job?

- Have you or your family experienced an unexpected medical expense, or any other major financial set-back?

- Are you behind on any payments, or are you still current?

- Are you still paying the HOA dues, if any?

- Are you still paying utilities like water, sewer, trash and disposal? If not, are there any delinquent payments?

- Are you still occupying the property?

- If not, is the property vacant, or is/are there tenant(s) occupying the residence?

- Have you attempted a loan modification, or previously attempted a short sale?

- Has your bank issued a Notice of Default, and if so, have they scheduled a Trustee Sale Date?

These are just a few questions that will pertain to the listing, sale and success of your Beaumont Short Sale.

These are just a few questions that will pertain to the listing, sale and success of your Beaumont Short Sale.

If you have questions about a Beaumont short sale, how they work and the myriad of opportunities AND pitfalls a short sale can provide you, feel free to call us anytime at (888) 9-LIST-IT. That's (888) 954-7848.

We can answer your questions and provide you with an in-depth look at the short sale process. We are not salesmen. We will tell you like it is, and if a short sale is the right choice for your particular situation (and many times a short sale is not our recommendation). We will give you honest answers with your best interests in mind. Having the right California Short Sale Experts assisting you can mean the difference between a foreclosure, or a fresh start without complete devastation to your credit due to foreclosure.

So if you'd like more information on a Beaumont Short Sale, Call us now:

(888) 9-LIST-IT. That's (888) 954-7848.

Other Real Estate Blogs:

New Foreclosure Fund May Change Mod. Loans, Short Sales and Foreclosure Processes

CLICK HERE TO LIST AND SELL YOUR BEAUMONT HOME NOW

A ray of good news shined through the ominous clouds of the fiscal cliff this past week stating that the Mortgage Forgiveness Debt Relief Act has officially been extended. Through this act, homeowners who are involved in a short sale, foreclosure, or mortgage restructuring are able evade a significant tax bill.

However, the storm is not anywhere near from over. The recent fiscal cliff deal was a small step of progress but the federal deficit still needs to be resolved which calls for more budget battles ahead. Could we be seeing our last Mortgage Forgiveness Tax Relief Act extension in 2013?

Only hours before the end of year 2012, congress was able to strike a deal to avert the fiscal cliff. Fortunately, this included the extension of the debt relief act which is now set to the new expiration date: December 31, 2013. It is official and the proof can be found in the IRS Website or in the American Taxpayer Relief Act of 2012 Bill.

Homeowners are very fortunate to get one extra year of opportunity to short sell their homes. Congress realizes that without this extension, numerous homeowners would be devastated with critical financial conditions. Although, the extension of the various tax cuts alleviated our impending tax increases momentarily, our government is also in a bad financial position in that it has a debt ceiling issue to deal with and the $1.3 billion dollars in taxes that they lost through the extension of the act may be a provision that our government may not be able to continue in our future budgets.

We may get a better forecast in a couple of months as a debt ceiling battle in Congress may occur and more budgets will be established.

What are your thoughts on this? Do you believe we will get an extension beyond Jan 1, 2014?

***REALTORS - Recommend This Blog Post for being "Featured" on Activerain, as it will certainly help draw much more attention to this matter! Just log into activerain and click the "suggest" button at the top of the post! Share on social networks to help get the word out!

http://activerain.com/blogsview/3589527/government-controlled-natio...